- GritALPHA

- Posts

- A Full Analysis of Western Digital ($WDC)

A Full Analysis of Western Digital ($WDC)

The 450%+ gainer over the past year...

Hi everyone,

Today we’re be breaking down a company whose stock is up +450% over the last year. Yes… you read that correctly.

Let’s dive into Western Digital (ticker WDC).

Stock Deep Dive: Western Digital Corp. (WDC-US, $96B MCAP)

Western Digital is the quiet backbone of the AI boom.

Everyone talks about GPUs, but AI runs on data, and data has to live somewhere. As hyperscalers race to build AI factories, they also need “storage factories” to hold training corpuses, checkpoints, logs, and archives at massive scale.

WDC sits right in that slipstream, coming off a brutal storage downturn with a setup that can flip fast: if pricing firms and cloud orders normalize, margins and cash flow can rebound hard.

This is not a straight-line story, but it is a classic cycle-meets-secular trade where the next leg can surprise people who only watch compute.

Why Now? 👉 Data Storage in the Age of AI

Overview 👉 What Does Western Digital Do?

How Storage Fits into the AI Buildout

How Do They Win? 👉 Value Proposition

Business Units 👉 Segment Breakdown

How Do They Make Money? 👉 Revenue Model

By The Numbers 👉 Key Metrics

Competition and Outlook

Risks 👉 Potential Pitfalls

What Makes this Biz Tick?

Wrapping Up…

Why Now? 👉 Data Storage in the Age of AI

Western Digital (WDC) is at an inflection point where a cyclical rebound is colliding with a secular AI storage tailwind. After the 2022–2023 storage downturn, investors began to price in improving supply-demand, especially as NAND pricing stabilized and cloud inventory digestion eased. WDC’s valuation recovered alongside the narrative that AI infrastructure is not just GPUs, it is also massive data storage. Strategically, WDC is also reshaping itself: after Kioxia merger talks stalled, the company announced plans to separate into two businesses (HDD and Flash), aiming to sharpen focus and unlock value.

Recent results show the “bottoming” pattern investors look for in cyclicals: fiscal Q1 2024 revenue of $2.75B was down 26% YoY, but up 3% sequentially, with a GAAP net loss of $685M. Management commentary pointed to improving client and consumer trends and a more constructive cloud outlook as qualification of higher-capacity drives expands. The setup is simple: if pricing improves and hyperscaler demand normalizes, WDC has meaningful operating leverage.

Overview 👉 What Does Western Digital Do?

Western Digital is a global data storage manufacturer spanning two core technologies: hard disk drives (HDDs) and NAND flash-based storage. In plain terms, it builds the “containers” where the world’s data lives, from consumer external drives and memory cards to enterprise-grade data center drives. The WD and SanDisk brands give it broad reach across retail channels, while its enterprise products serve hyperscalers and large IT customers.

WDC’s HDD business focuses on high-capacity drives used in data centers and bulk storage, where cost per terabyte is the dominant buying criterion. Its flash business includes client SSDs, enterprise SSDs, removable storage (USB, SD, microSD), and embedded flash in devices. A defining feature is vertical integration in flash through its long-standing joint venture with Kioxia, which supports NAND manufacturing scale and technology development.

For a general audience: when you back up a laptop, store photos on a memory card, or when a cloud provider stores training datasets for AI, WDC’s products are often in the stack. The company’s role is foundational, but its results swing with storage pricing cycles and customer capex patterns.

How Storage Fits into the AI Buildout

AI is a storage story as much as it is a compute story. Training and operating modern models requires vast datasets, repeated checkpoints, logs, and archives. The fastest GPUs in the world are useless if data cannot be staged, moved, and retained efficiently. This is where WDC’s product mix maps cleanly into the AI buildout.

First, nearline enterprise HDDs are the bulk capacity backbone of cloud storage. Hyperscalers need the lowest cost per terabyte for multi-petabyte training corpuses and long-lived archives, which keeps HDDs structurally relevant even as SSDs expand. WDC’s high-capacity nearline drives (22TB to 26TB class) are designed for exactly this use case and have been qualified across major cloud customers, positioning shipments to scale as cloud ordering improves.

Second, NVMe SSDs and flash play the speed layer. AI training pipelines often stage “hot” datasets on fast SSDs to keep accelerators fed, while inference and edge deployments can require local flash storage for models and data. Third, compliance and reproducibility increasingly require retaining raw data and model versions, reinforcing demand for archival storage. Net effect: AI expands the total storage footprint across performance tiers, and WDC participates across both capacity and speed layers.

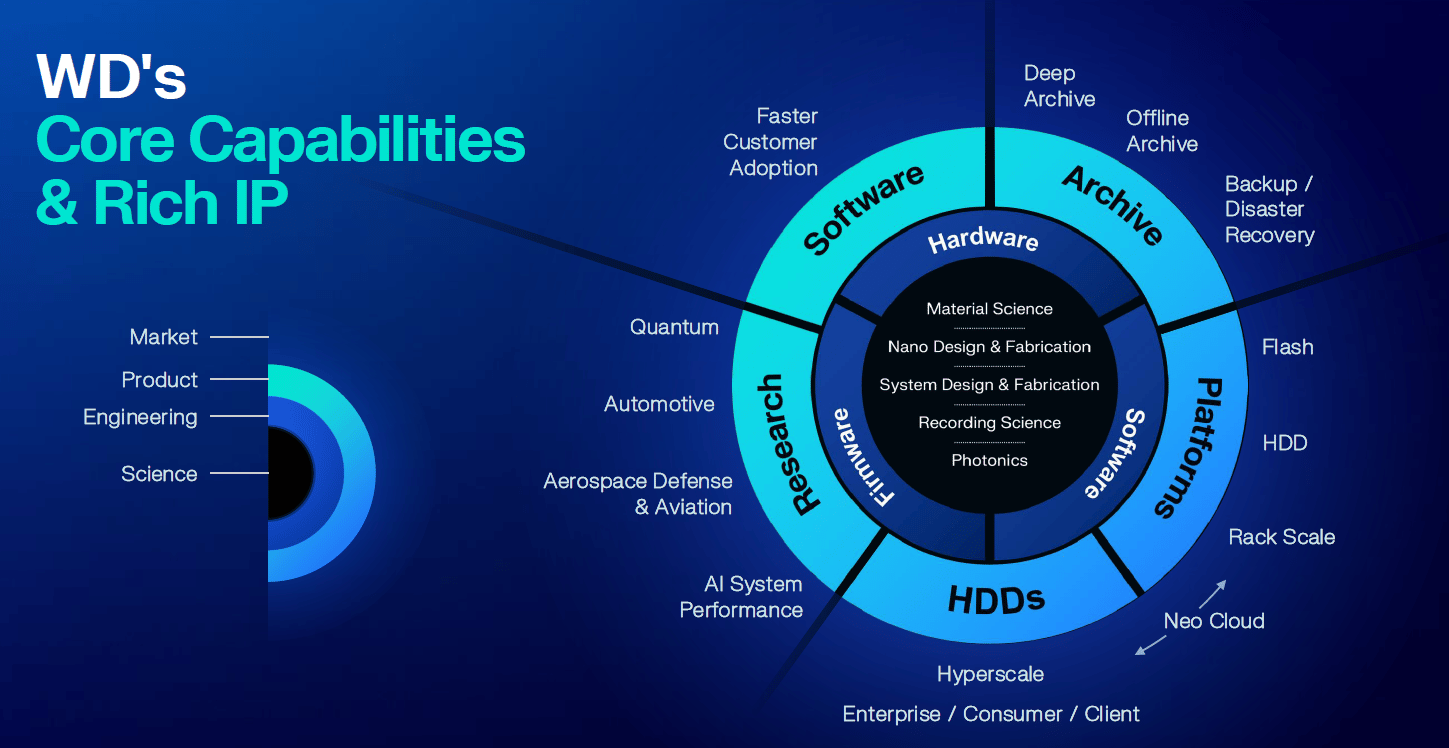

How Do They Win? 👉 Value Proposition

Source: Company Filings

WDC’s “win” condition is straightforward: stay on the cost and technology frontier while maintaining disciplined supply and strong customer qualification. Its differentiator is breadth across HDD and NAND, enabling it to serve both bulk-capacity and performance-oriented storage needs. In flash, vertical integration through the Kioxia JV supports supply security and cost competitiveness versus vendors that must buy NAND on the open market.

Technology execution is central. In HDD, the ability to deliver higher capacities (ePMR, SMR, UltraSMR roadmaps) and earn hyperscaler qualifications drives share and pricing power at key inflection points. In flash, advancing 3D NAND generations (BiCS roadmap) and pairing with competitive controllers and firmware matters for enterprise SSD design wins and cost per bit.

Operationally, WDC’s scale lets it cut costs aggressively in downturns and expand margins sharply when pricing turns. Brand strength (WD, SanDisk) supports consumer channel reach and mix benefits. The planned separation into HDD and Flash businesses is also part of the “win” strategy: simplify operating models, improve transparency, and potentially unlock valuation through sharper segment narratives and strategic optionality.

Business Units 👉 Segment Breakdown

Source: Company Filings

WDC operates two major segments: HDD and Flash. The HDD business is anchored by nearline enterprise drives for cloud and data center customers, where WDC competes in a tight market structure (primarily versus Seagate, with Toshiba smaller). HDD demand is driven by exabytes shipped and capacity-per-drive trends, and profitability tends to be steadier given fewer industry players and more controlled supply.

The Flash segment spans NAND components via the Kioxia JV, client SSDs for PCs, enterprise SSDs for data centers, and removable storage under the SanDisk brand. Flash is structurally more volatile because pricing can swing sharply with industry supply additions, but it also benefits from secular growth in content per device (more GB in phones, PCs, and cloud SSD footprints).

End markets typically break into Cloud (hyperscalers and enterprise), Client (PCs, devices, consoles), and Consumer (retail channel). In downturns, mix can shift materially as hyperscaler ordering pauses or resumes, which is why WDC’s results can change quickly. Looking ahead, the planned split formalizes what the market already knows: HDD and Flash behave like different businesses with different cycles, competitors, and investor bases.